The 1975 Five-Part Test Is Back: What Financial Advisors Must Do when working with “held-away” 401(k)s

The 1975 “five-part test” returned this year, and if you think that means less risk, pump the brakes.

After the March 2026 court decisions wiped out the DOL’s 2024 Retirement Security Rule, the Department of Labor (DOL) officially reverted to the old standard.

Sounds simple?

It’s not.

For advisors handling . . .

Three Rulings, One Message: Why Documenting Your Fiduciary Process Is the Only Defense You Need

In the high-stakes world of ERISA litigation, many financial advisers believe that their primary job is to deliver superior investment returns. They are wrong. While clients certainly want growth, the legal reality of the Employee Retirement Income Security Act (ERISA) is far more rigid…

The Ultimate Guide to "Held-Away" 401(k) Advice: Staying Compliant While Growing Your Practice

Let’s be real: few things are more annoying for an advisor than seeing a big chunk of a client’s wealth trapped inside a 401(k) you can’t directly manage. You’re building a financial plan with one hand tied behind your back. You can’t see the fund lineup their employer chose, the stale allocations, or the lack of rebalancing.

And the second you start talking about managing it? Compliance starts sweating.

You’re not crazy. Held-away 401(k) advice really is one of the messiest corners of wealth management . . .

Alts in the 401(k): Navigating the DOL's New Rule on Private Equity and Crypto

If you’ve been in the retirement game for more than five minutes, you know that the "Goldilocks" portfolio, that 60/40 split of stocks and bonds, has been looking a little dusty lately.

For years, financial firms have been staring longingly at the returns generated by institutional players in the private equity and crypto markets, wondering, "Why can’t my 401(k) clients have a slice of that?"

Well, the Department of Labor (DOL) just dropped a bombshell…

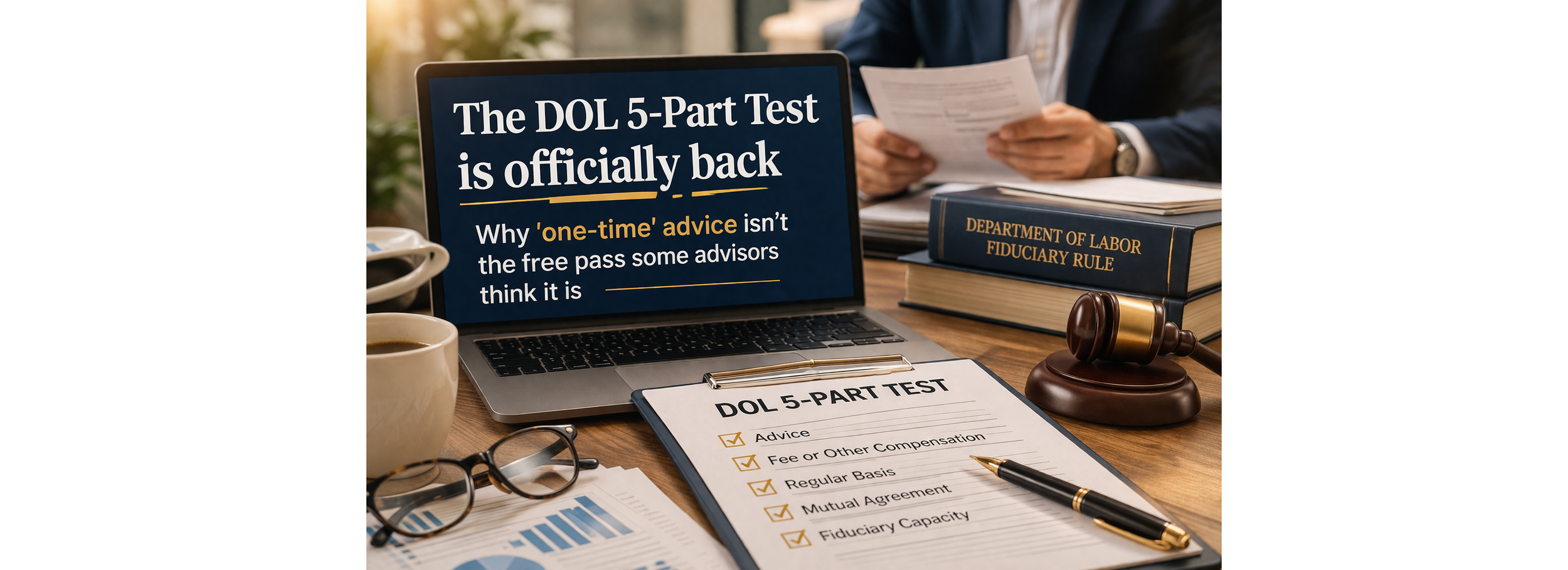

The DOL 5-Part Test is officially back , Why 'one-time' advice isn't the free pass some advisors think it is

Well, here we are. It’s March 2026, and if you feel like you’ve been caught in a legal time machine, you aren't alone.

The whiplash is real!!

After years of legal gymnastics, the 2024 Biden-era Retirement Security Rule has been vacated by the courts, and the Department of Labor (DOL) has officially retreated to the 1975 trenches….