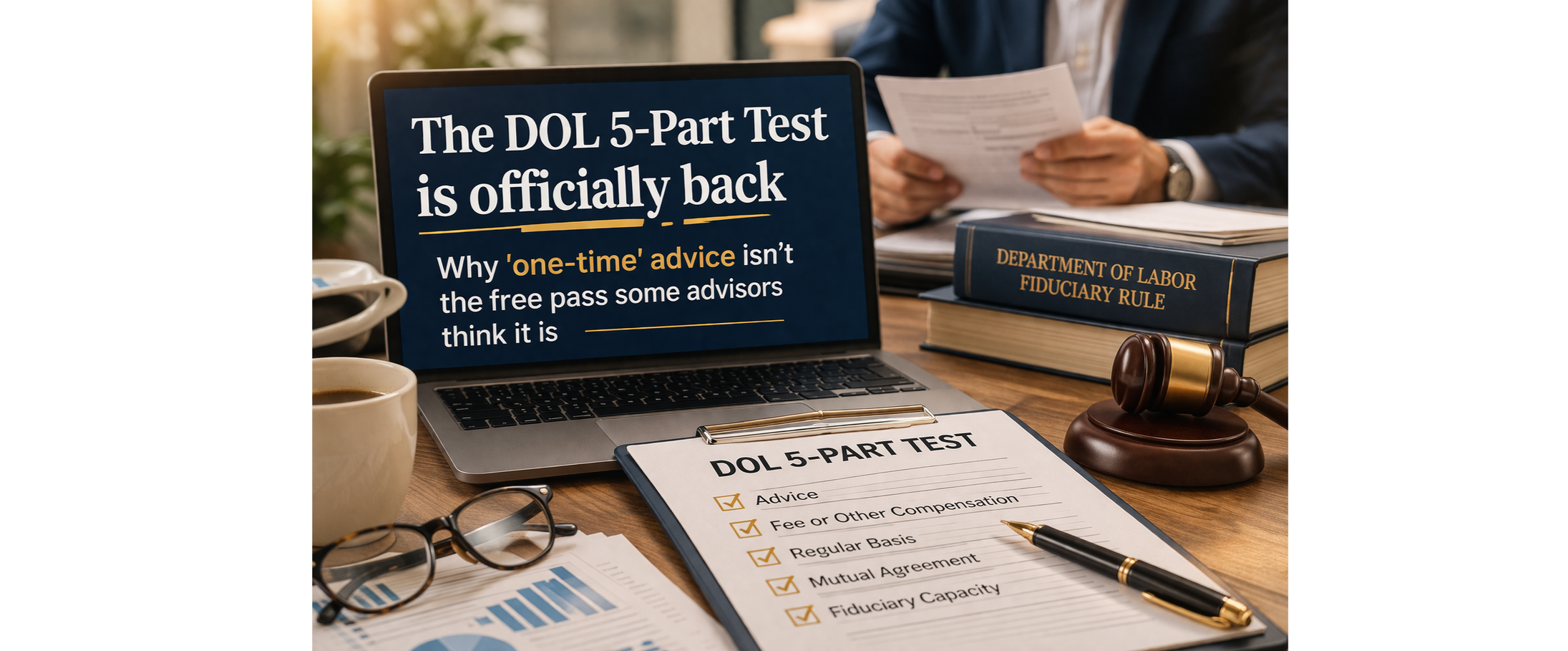

The DOL 5-Part Test is officially back , Why 'one-time' advice isn't the free pass some advisors think it is

Well, here we are. It’s March 2026, and if you feel like you’ve been caught in a legal time machine, you aren't alone.

The whiplash is real!!

After years of legal gymnastics, the 2024 Biden-era Retirement Security Rule has been vacated by the courts, and the Department of Labor (DOL) has officially retreated to the 1975 trenches.

We are back to the Five-Part Test (again).

For some of you, there was a massive sigh of relief. You’re thinking, "Great! We can go back to the way things were. One-time rollover advice is safe again. I don't have to be a fiduciary for that initial transaction!"

I hate to be the one to rain on your compliance parade, but I have to play devil’s advocate here.

If you think the return of the Five-Part Test is a "get out of jail free" card for rollover recommendations, you are standing in a field holding a lightning rod during a thunderstorm.

Let’s nerd out on why that "one-time" advice defense is a lot flimsier than you think.

The Anatomy of the 5-Part Test (The "Old-School" Standard)

To be considered a fiduciary under the 1975 rule, a person must meet all five of these criteria. If even one is missing, you aren't an ERISA fiduciary. (On paper, anyway).

Value: You render advice as to the value of securities or other property, or make recommendations as to the advisability of investing in, purchasing, or selling them for a fee.

Regular Basis: You provide this advice on a regular basis to the plan or participant.

Mutual Understanding: The advice is given pursuant to a mutual agreement, arrangement, or understanding.

Primary Basis: The advice will serve as a primary basis for investment decisions.

Individualized: The advice is individualized to the specific needs of the plan or participant.

In the "good old days," advisors used the "Regular Basis" prong like a shield.

They argued that a rollover is a one-time event.

You meet the participant, you suggest they move their 401(k) to an IRA (which you happen to manage), and boom: transaction complete.

Since it wasn't "regular," it wasn't fiduciary advice.

Head spinning yet?

It should be. Because the DOL’s interpretation of "regular" has evolved, even if the rule itself just went back to 1975.

The "Regular Basis" Trap: It’s Not a One-Night Stand

Here is where it gets spicy. The DOL has previously clarified (and they haven't exactly deleted these thoughts from their collective brain) that a single instance of advice can be the beginning of an ongoing relationship.

If you are currently working with the plan or participant, and then you recommend a rollover and you sign that individual up for a wealth management agreement where you provide ongoing management, that "one-time" rollover may not be deemed the first step in a "regular" relationship.

You can’t be an ERISA Fiduciary (providing current services) and then just put on a "Non-Fiduciary" hat for the rollover and then swap it back for a "Fiduciary" hat ten minutes later once the assets hit the IRA.

The DOL (and more importantly, the trial lawyers) will look at the intent and the totality of the relationship

.

And if you are not sure if you were an ERISA Fiduciary PRIOR to the rollover, check out our deep dive on am I an ERISA fiduciary for more context on how these definitions bleed into each other.

Why "Primary Basis" is Harder to Dodge Than You Think

The fourth prong of the test requires that the advice serves as a "primary basis" for the investment decision.

Some advisors think that if the client talks to their spouse, their brother-in-law, or reads a couple of articles on Reddit, the advisor’s advice isn't the "primary" basis.

Wrong.

The DOL has made it clear: "Primary" doesn't mean "exclusive." If your advice was a significant factor that determined the outcome of the decision, you’ve likely met this prong.

In the eyes of a regulator, if a participant moves $500,000 because of a presentation you gave, you were most likely the primary basis.

The Reality of Litigation Risk (The "Nerd" Warning)

Even with the Biden rule vacated, the environment for financial advisors hasn't magically become "safe."

We are living in an era of unprecedented ERISA litigation.

Plaintiffs' attorneys are smarter and more aggressive than ever. They don't care if the 1975 test is back; they care about fiduciary breaches.

If you move a client out of a low-cost 401(k) plan with institutional pricing into a retail IRA with higher fees and proprietary products, you could have a target on your back.

And let’s talk about "held-away" assets.

Whether you're using 3rd party tools to manage assets inside a 401(k) or if you're advising on these assets for a fee, you can easily be in the crosshairs. (This is why the largest financial firms don’t get involved with “held-away” 401(k) assets. This is a HUGE opportunity for Independent Advisers that do it properly)!

You should probably check out our post on why there is going to be an increase in ERISA lawsuits.

Best Practices: Don't Play the "Maybe" Game

Now that we've covered why the "one-time" defense is mostly a myth, what should you actually do?

How do you protect your practice in this "back to the future" regulatory landscape?

Assume Fiduciary Status: Honestly, the safest way to run a business in 2026 is to act as a fiduciary in all retirement-related recommendations. It’s better to have a process that meets the highest standard (PTE 2020-02) than to try and "pencil out" exactly how much non-fiduciary advice you can get away with.

Document the "Why": If you recommend a rollover, you need to document why it's in the client's best interest. Compare fees, compare services, and compare investment options. If you can’t prove it’s better for the client, why are you doing it? (Aside from the obvious AUM boost, which: spoiler alert: is not a valid fiduciary reason). This is required by PTE 2020-02 and Reg BI. So, just do it!

Review Your "Processes": ERISA requires you to have prudent written processes for advising, trading and rolling over assets. Then you must follow your written process each and every time and document (kept for six years) that you followed it. You should review your processes each year. In fact PTE 2020-02 requires a written retrospective review and certification six months after you year end.

So, this one is not optional.

The Bottom Line: My Two Cents

The return to the 5-part test feels like a win for those who want less red tape.

But in reality, it creates a "gray area" that is confusing and frustrating since ERISA was never written with 401(k) assets/participants in mind.

"Gray areas" in compliance are where firms go to die.

If you are treating a rollover as a "one-time" non-fiduciary event while simultaneously providing that same client advice/trading for their 401(k), you are handing out lit matches in a fireworks warehouse.

You’re not crazy for feeling frustrated by the constant rule changes.

Every presidential administration since George W Bush has been trying to modernize the ERISA law / DOL Rules.

But don’t let frustration lead to complacency.

Stay nerdy, stay compliant!

Want to make sure your firm isn't the next headline in an ERISA lawsuit? Check out our best practices for 401(k) fiduciary advisors.